Yesterday, I became reacquainted with “hack” – a harsh bit of a word. On the one hand, hack is when you take big chops into a tree with your ax. Nothing wrong with that. Hack is also whether you can cope with a given situation (i.e. “can you hack it?”). Nothing wrong with that either. But then again, hack is uncontrollable coughing caused by a bad cold. Or even worse, hack is breaking into a computer or account, with not-so-nice intentions.

I experienced not-so-nice hack yesterday. My wife and I are waging war with a cold we’ve had since Easter. Together we’re coughing up a storm (sounds of thunder). More to the subject at hand, our bank left a tidy little message on our answering machine last night. “…do we have reason to suspect fraudulent charges on our Visa card?” So, I logged onto our account and scrolled down to the last couple of days of activity. There the little devils hid – six small charges, all for the food-delivery service “DoorDash“.

Have I ever used DoorDash? (No.) Do I even know what DoorDash is? (I do now.) I have no use for DoorDash, nor them for me. We live in the country; wide, open spaces in every direction. The only way we get pizza delivery is to agree to meet the driver halfway. The only way we get trash service is to pay “fuel surcharges” on top of the monthly bill. We’re too far out for DoorDash. Just for grins, I entered our address into DoorDash’s website and up popped my options. Cool! For thirty days I get free service on delivery orders above $10. Not cool – I have zero nearby restaurants offering DoorDash. Guess its pizza for dinner again tonight.

But I digress. Back to the hack. To my bank’s “credit”, they handle minor fraud efficiently. They noticed the hack before I did (bless their computer algorithms). Once I called back and denied any knowledge of DoorDash, they blocked my card and promptly dropped a new one into the mail. A few days from now, I’ll be off and charging again, the only real inconvenience being to update my linked accounts.

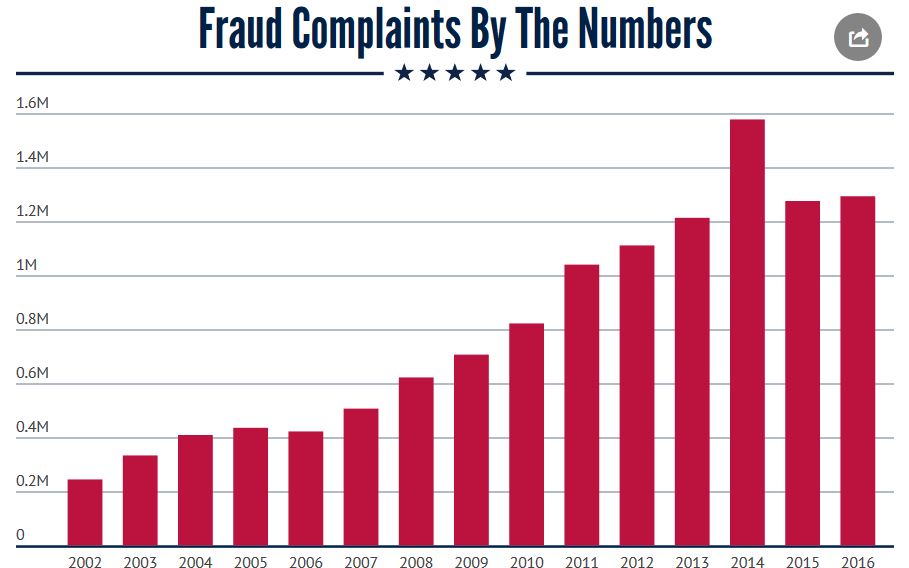

I wish I could leave it at that. After all, this incident won’t cost me a penny. Those who pay annual fees and interest charges unknowingly pay the cost of credit card fraud as well ($40 billion every year). I just can’t get past the fact someone out there enjoyed six free DoorDash deliveries courtesy of my credit.

The scammers are winning this game hands-down. A physical credit card allows crazy-easy access to its critical information. Take your pick as you regularly surrender your data: 1) through your phone, 2) through your computer, 3) through self-service devices (i.e. gas pump, ATM), and 4) by simply handing over your card at a place of business.

My DoorDash friend picked up my numbers through one of the last two ways – I’m sure of it. I never give out my credit card over the phone, and the websites I use have some form of verifiable security. Alas, self-service devices and handing over cards are no-win situations. With the former, you encounter skimmers (discrete data-collection devices placed over card readers). With the latter, you risk the merchant or waitstaff copying your numbers when out of sight. They probably use a skimmer as well.

The only real solution to credit card fraud – sad to say – is not using the card at all. Pay for your gas with cash. Write a check for the cash you would’ve taken out of the ATM. Technology is improving the situation (i.e. Apple Pay, table-side pay systems), but until these approaches become the norm, you’ll continue to deal with situations where your card goes out-of-sight.

The only real solution to credit card fraud – sad to say – is not using the card at all. Pay for your gas with cash. Write a check for the cash you would’ve taken out of the ATM. Technology is improving the situation (i.e. Apple Pay, table-side pay systems), but until these approaches become the norm, you’ll continue to deal with situations where your card goes out-of-sight.

Frankly, I’m not asking for much here. All I want is my bank to collar my DoorDash friend and let me know he/she faces the consequences of their actions. But I know my little scammer is not worth their time. Instead, he/she keeps getting free food, and annual fees and interest rates tick up a little bit more.

Frankly, I’m not asking for much here. All I want is my bank to collar my DoorDash friend and let me know he/she faces the consequences of their actions. But I know my little scammer is not worth their time. Instead, he/she keeps getting free food, and annual fees and interest rates tick up a little bit more.

My brand new Visa card arrives later in the week. I’ll activate it and update my linked accounts. The inconvenience to me amounts to less than thirty minutes. But the annoyance of it all – well – that feeling lasts a whole lot longer. I just hope, by the time DoorDash gets to my neighborhood, I’m no longer perturbed and willing to give it a try.

Hope they’ll take cash.

Some content sourced from the March 2019 Upgraded Points article, “The Best Ways to Prevent Credit Card Fraud & Theft”.

That’s terrible. Glad you caught it quickly. I haven’t heard of DoorDash.

LikeLike

I’ve never heard of DoorDash either, but often will use cash, and go to the teller instead of the ATM just to avoid using my card. I have had the bank call and verify unusual activity and then wonder if even that call is legit or is a scammer trying to get info!

LikeLiked by 1 person

Our bank lets you use your phone instead of a card at the ATM, so I use that these days to avoid the skimmer problem. And I still use cash, particularly for purchases under, say, $20. But I still use credit cards at the gas station, so I’m vulnerable there. Oh, and my wife and I got a credit card just for recurring charges: all of the linked accounts go on that card, and then the card is stashed in our home safe — it is never used for anything else. That way, if one of the cards we carry is compromised, we don’t have to update the linked accounts. And because we only allow a limited set of merchants — ones we actually trust — to see that special credit card, the likelihood that it’ll be compromised is fairly low. This strategy has been working well for a couple of years now.

Now if we could just get all of the merchants to update their equipment to use the chip on the card, rather than the magnetic stripe, we’ll be a little bit safer. I would especially love it if all of the restaurants did the European thing and handled your credit card transaction entirely at your table: their system of never taking your card out of your sight seems so logical and so sensible that, aside from the fact that restaurants would be forced to pay a one-time charge for the equipment, is a no-brainer in my mind.

Oh, and finally, we do use DoorDash, albeit very occasionally. It seems to work fairly well in an area with short driveways and plentiful restaurants.

LikeLiked by 1 person

A couple of really good suggestions there – thanks. I didn’t realize I have the card-free option for ATMs! I’ll have to give that a try.

LikeLike